Trump Filings - A Deep Dive

Let's find out what all the excitement is about

Have you noticed the prolification of accounts posting Trump trades on X? Some have even been banned. Retail investors are obsessed with it because they think its a source of alpha. Well lets find out if they are correct…

I ran a backtest on 600+ stock purchases disclosed in presidential financial filings. The results are interesting. The caveats matter just as much as the numbers.

Presidential financial disclosures exist to prevent conflicts of interest. The practical side effect is that they create a public record of trades made by the most powerful market participant in the world. We built a backtest to find out whether that record is actually actionable.

The short answer is that it appears to be. The longer answer is more complicated.

The Methodology

The dataset covers roughly 625 stock purchase transactions disclosed in executive OGE Form 278-T filings from January 2025 through May 2026. These are the executive branch equivalent of congressional STOCK Act disclosures - required for senior officials including the President.

I built two models and ran them side by side.

Theoretical - Enter on the transaction date, exit N days later. This is the theoretical upper bound: you somehow know the trade happened the day it was made. It is unrealizable. No one outside the White House knows when these trades occur.

Copy-Trade - Enter on the filing date, exit N days later. This is the realistic version. You read the disclosure when it becomes public and buy the same stocks the following morning.

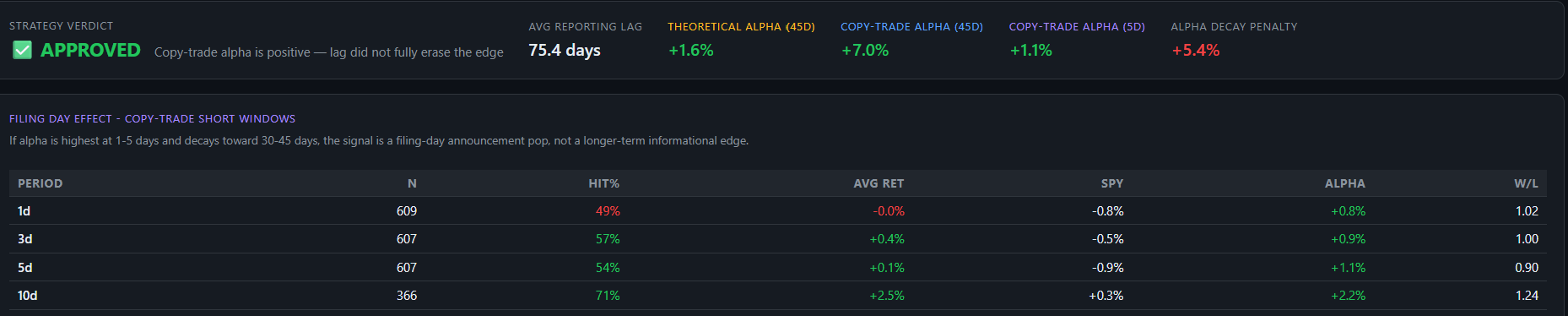

The average reporting lag in this dataset is 75.1 days. The legal maximum is 45 days. So by the time you can act on any of these filings, more than two months have already passed since the actual trade.

The Main Finding

The copy-trade model at 45 days outperforms the theoretical model at 45 days. By a lot. The follower beats the insider by 5.4 percentage points. That should not happen if the edge is informational - if it were, the reporting delay would only destroy alpha, not create it.

The most plausible explanation is timing. The bulk of these trades were executed during the February-March 2025 tariff sell-off. Trump’s original entry dates landed during the drawdown. Copy-traders, entering 75 days later, were effectively buying the recovery. The alpha in the copy-trade model is probably a market-timing artifact from an unusual macro cycle, not an ongoing structural edge.