Rocket Lab (RKLB)

A Rhodie House Options Intelligence Study

I posted this article in my discord this morning at around 8 am.

Today I purchased RKLB stock pre-market and on the cash market open.

Reading the Flow: Why the Notes Column Is What Matters

RKLB Case Study | Rhodie House Options Intelligence | April 2026

One question that comes up from time to time is how we determine whether a trade is bullish or bearish, and why that conclusion sometimes differs from the raw exchange label shown on the option chain.

The short answer is this: the CBOE execution label — whether that is “Puts Bought,” “Calls Sold,” or similar — reflects where the trade printed relative to the bid-ask spread at the moment of execution. It does not always tell you the direction of the trade. For single-leg, straightforward flow, the two usually line up. For multi-leg structures, and particularly for crossed trades, they often do not.

A note on the dashboard and Discord. The Type column in the flow dashboard shows the raw CBOE execution label exactly as reported. The Notes column shows the curated classification, and it is Notes that determines how the trade is described in the #live-option-flow Discord channel. The two are the same: what you see posted in Discord is pulled directly from Notes. Classification happens as the trade comes in, in real time. In the case of the April 8th trade below, the SPRD/CROSS/TIED condition and the millisecond-matched legs warranted a closer look before fully committing to direction. Once the associated stock sale was confirmed, the Notes entry was amended from the initial bearish classification to bullish risk reversal. That is the only amendment in this case. The April 10th trade was classified correctly at the time it came in and was not changed.

RKLB this week is a textbook example.

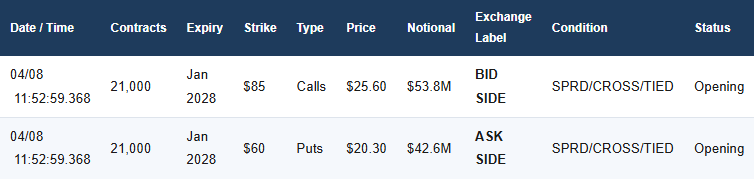

April 8th — The Initial Trade

At 11:52:59 on April 8th, a 21,000-contract risk reversal hit the tape simultaneously in the Jan 2028 $85 calls and $60 puts. Both legs printed at the exact same millisecond, both marked Opening, both on PHLX under a SPRD/CROSS/TIED condition.

The raw CBOE labels showed the calls at the bid and the puts at the ask. On paper, that reads as calls sold and puts bought — a bearish risk reversal. That was the initial classification. However, the same millisecond timestamp on both legs and the SPRD/CROSS/TIED condition signaled that this was a packaged cross, not open market flow, and warranted a closer look before committing to direction.

The Stock Sale

Fifty-six seconds after the options printed, 1.89 million shares of RKLB traded on FINRA-ADF at $69.65 — roughly $132 million of stock moving off-book in the same window.

When you look at the options and the stock together, the picture changes completely. An institution selling $132 million of stock while simultaneously buying puts and selling calls would mean doubling down on a bearish thesis from two directions at once — that is not how accounts of this size operate in a single coordinated transaction. What actually happened is that the account sold its stock position and replaced the exposure with a bullish risk reversal: puts sold and calls bought.

In a crossed package of this kind, the bid and ask labels are reported from the perspective of the facilitating broker-dealer, not the end client. The direction appears inverted. This is not unusual for large institutional crosses and is one of the reasons the exchange label alone is never the final word on direction.

Confirmed read. Stock sold. Calls bought. Puts sold. This is a bullish risk reversal built as a stock replacement trade. The exchange type was inverted due to the mechanics of the cross. The Notes record was updated accordingly.

April 9th Open Interest — Confirmation

The April 9th open interest data confirmed both legs. The Jan 2028 $60 puts added 20,781 new contracts and the $85 calls added 20,793 — near-complete follow-through on both sides of the 21,000-contract trade. Both legs executed predominantly at mid-market, consistent with a crossed institutional package. The prior OI in both strikes was modest, which makes the scale of the new positions all the more significant.

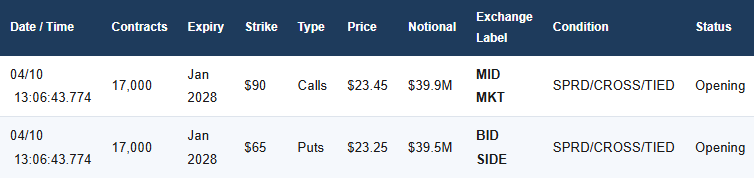

April 10th — A Cleaner Signal

A separate, unrelated risk reversal followed on April 10th. At 13:06:43, 17,000 contracts printed simultaneously in the Jan 2028 $90 calls and $65 puts — again at the exact same millisecond, both marked Opening, both on PHLX under a SPRD/CROSS/TIED condition. This time there was no associated stock sale.

The puts executed at the bid — puts sold — with the calls at mid-market, which is standard for a packaged cross of this size. No ambiguity on direction. Going into the trade, open interest in the $90 calls stood at just 4,599 contracts and the $65 puts had only 973. A 17,000-contract opening position against that backdrop is significant.

Classification. Puts sold at the bid. Calls at mid in a packaged cross. Both Opening. No stock component. Straightforward bullish risk reversal. This trade stands on its own.

April 10th Open Interest — Confirmation

The April 13th open interest data confirmed both legs. The Jan 2028 $90 calls added 16,968 new contracts and the $65 puts added 16,636 — near-complete follow-through on the 17,000-contract trade.

Why 2028 LEAPS — The Supporting Thesis

From a trading perspective, both of these trades make sense as bullish positions when you look at what is happening in the sector right now. The SpaceX IPO filing has reignited optimism across commercial space, and rotating into RKLB is one of the more logical ways to gain exposure to the sector ahead of what could be a blockbuster offering. The 2028 LEAPS in particular are worth understanding in that context.

SpaceX is targeting a valuation in the range of $1.75 trillion to $2 trillion. RKLB is currently trading in the $67 to $72 range. That gap is prompting analysts to re-evaluate where RKLB should be priced as the commercial space economy gains mainstream institutional recognition. The 2028 expiry captures the window where that re-rating has time to play out, and where Neutron — RKLB’s medium-lift rocket — is expected to be fully operational and competing directly for the market share that SpaceX’s public entry will validate.

There is also a scarcity argument. RKLB is one of the very few publicly traded names with proven medium-lift capability. When institutional capital wants listed space exposure, the options are limited, and that dynamic is showing up in the flow. The company’s fundamentals are providing additional support: backlog grew to $1.85 billion by early 2026, underpinned by a landmark $816 million SDA contract and a potential $700 million NASA Mars network bid. These are not speculative numbers — they represent contracted revenue and a pipeline that extends well into the LEAPS window.

Sector re-rating: SpaceX’s $1.75T-$2T target valuation prompts a fresh look at RKLB’s relative pricing.

Strategic scarcity: Few listed names with proven medium-lift capability. Institutional capital has limited places to go.

Backlog: $1.85B, including $816M SDA contract and potential $700M NASA Mars bid.

Neutron timing: 2028 LEAPS capture the window of full Neutron operability and direct market competition.

The Starlink listing, when it comes, will validate the commercial space economy more broadly and is already creating a “buy the sector” sentiment that benefits names like RKLB, ASTS, and PL. That said, there is a counterpoint worth acknowledging. Once SpaceX shares are actually available to buy, some capital that is currently sitting in listed proxies may rotate directly into SpaceX, which could create a headwind for smaller names. That is not a reason to dismiss the thesis, but it is a factor to keep in mind when sizing and timing any position.

What This Means

The Notes column in the dashboard reflects a curated read on each trade, not a mechanical pass-through of the exchange label. The underlying trade record is never changed, but every trade that comes through is classified based on the full picture: structure, open interest changes, execution conditions, and additional context where it can be obtained. The exchange label is a starting point, not a conclusion. When the Notes say bullish or bearish, that reflects genuine work, not a flip of the bid-ask coin.

I will not guess. If a trade is not clear, I would rather dig deeper, query exchange records, or consult with people who have more information before attaching a direction that is not supported by the evidence. In the case of the April 8th RKLB trade, the initial exchange label suggested bearish. The stock sale record, the logic of the structure, and the open interest confirmation all pointed the other way. The Notes were updated once that picture was complete.

That said, while the evidence in both trades points to bullish intent, I could be wrong. No analysis of this kind comes with a guarantee, and there are always factors that are not visible from the outside. What matters is that you look at the facts available, weigh them carefully, and make your own determination. The work we do here is intended to give you a better starting point, not to replace your own judgment.

The April 10th follow-on trade is a good illustration of what clean, unambiguous flow looks like by comparison. Both are worth watching going into earnings season.

Now tell me what other options service gives you this level of curated flow? This is where the alpha lives.

Thank you for posting this, Judah. I am grateful for the opportunity to learn from you.