Portfolio Hedging, Simplified

Rhodie House Options Intelligence

Most traders know they should hedge their portfolio. Most do not know how many contracts to buy.

The answer is not a round number you pick based on feel. It is a calculation. It depends on the beta of every stock you hold, the delta of every option, and how much of your total market exposure you actually want to offset. Get any of those wrong and your hedge either costs too much or does not work when you need it.

I built a tool that does the math for you.

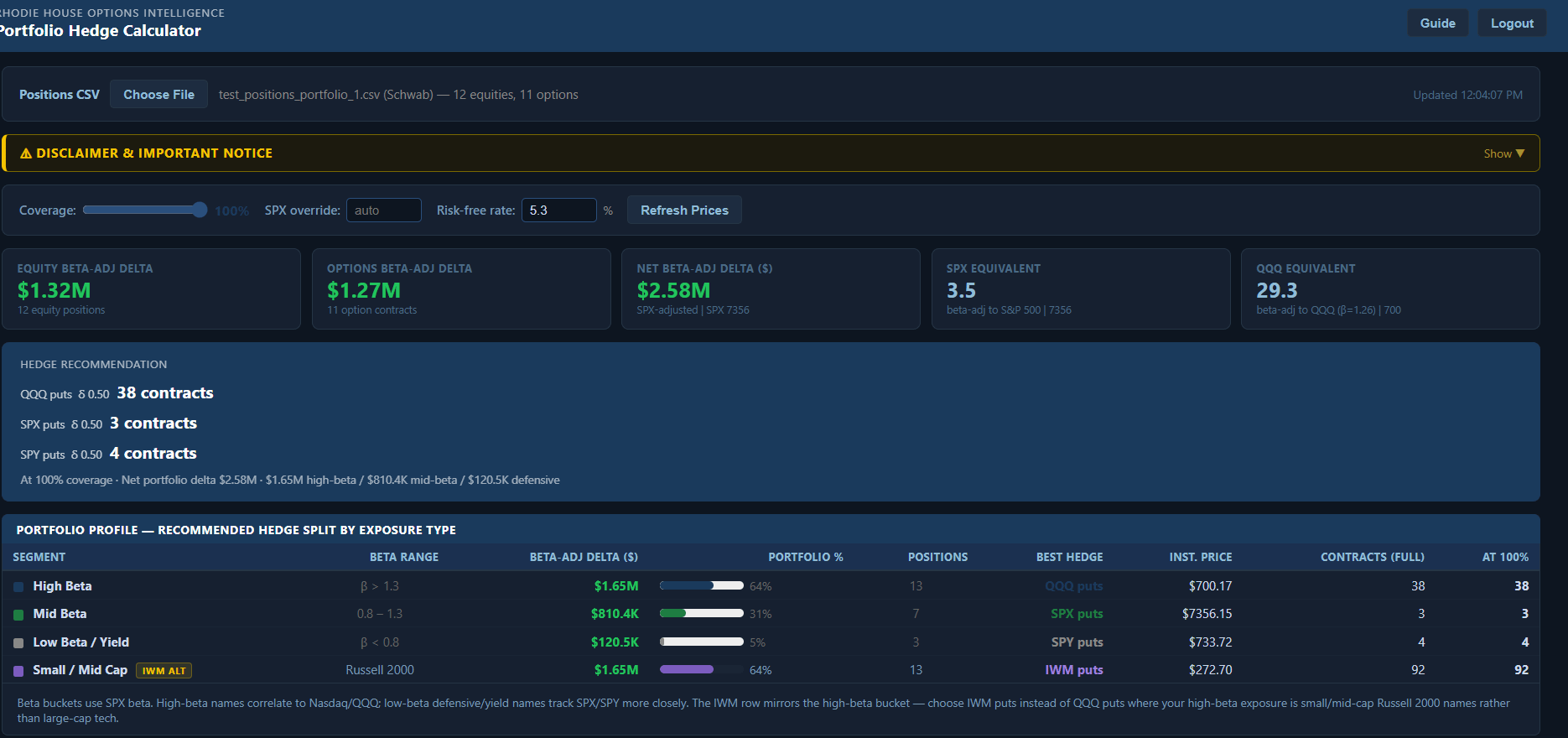

What It Does

Load your positions file and the calculator converts every stock and option in your book into a single number: your true net exposure to the S&P 500, in dollar terms, beta-adjusted and delta-weighted. From that number it calculates exactly how many contracts you need on SPX, SPY, QQQ, or IWM to offset it at any coverage level you choose. The tool accepts CSV exports from Schwab, IBKR (Flex Query), and Fidelity — load the file, no reformatting required.

It accounts for everything. Long stock. Short stock. Long calls. Long puts. Covered calls. Spreads. Every position contributes to the total, with the correct sign and the correct weighting.

The Right Instrument for Your Book

Hedging a tech-heavy portfolio with SPY puts is a common mistake. When the Nasdaq drops 4% and SPY drops 2.5%, your hedge underdelivers. The tool splits your portfolio into four segments and recommends the instrument that most closely tracks each one.

High-beta growth names point to QQQ puts. Broad market names point to SPX puts. Low-beta dividend names point to SPY puts. Small and mid-cap names point to IWM puts, because the Russell 2000 has its own correlation profile and deserves its own hedge.

The contract counts update instantly as you adjust your coverage target and put delta. Change the slider, change the delta input, and the numbers recalculate in real time.

Built for Members

This tool is part of the Rhodie House Options Intelligence platform, available to paid Discord members alongside the live options flow dashboard, signals scoring, the index volatility suite, and the rest of the toolkit I have built for active options traders.

Your positions never leave your browser. The CSV is processed locally in the tab and no portfolio data is transmitted anywhere. Schwab, IBKR Flex Query, and Fidelity exports all load without any reformatting.