Following the Smart Money — The Option Strategies I Use and Why

Options flow is institutional intent made visible in real time. Every large, structured trade that hits the tape is a signal, not always clean, not always immediately obvious, but always worth understanding. After thirty-five years reading markets from the inside, I have come to believe that the most consistent edge available to an individual trader is not a proprietary model or a faster data feed. It is the discipline to watch what the largest and best-informed participants in the market are actually doing, understand why, and follow when the conditions are right.

Two strategies come through the flow repeatedly. I use both. And when the flow and the chart are aligned, its the kind of setup worth analyzing closely.

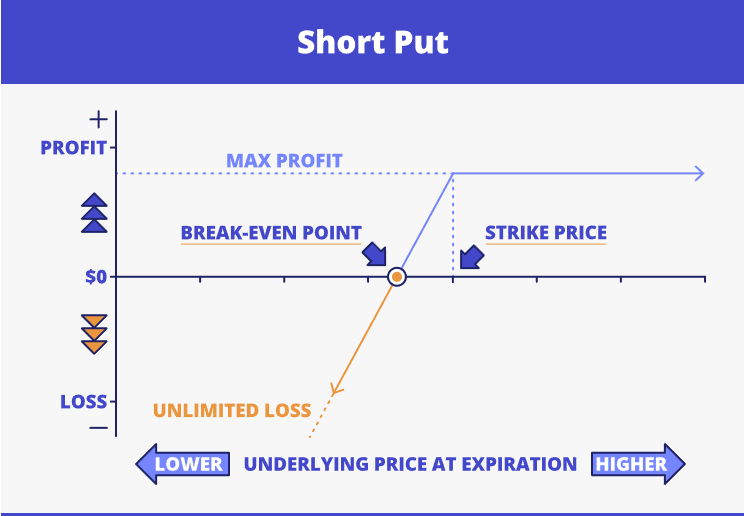

Selling Puts - Getting Paid to Wait

Selling a cash-secured put is one of the most practical tools in an options trader’s arsenal. The structure is simple: sell a put on a stock you are willing to own, collect the premium upfront, and set aside the cash to buy the shares at the strike price if assigned.

The trade has two outcomes. If the stock stays above the strike at expiration, the put expires worthless and you keep the premium - paid to wait for a price that never arrived. If the stock falls below the strike, you are assigned and buy the shares at the strike price, with your effective cost already reduced by the premium collected.

But the real power of this strategy is not the mechanics, it is what the flow tells you about where to sell. When institutional players are selling puts at a specific strike in size (large, structured, opening positions), they are revealing the price level at which they are willing to own the stock. These are not retail traders. They have done the fundamental work. They understand the business and they have sized accordingly.

When the chart confirms what the flow is saying, stock at a key technical level, institutional put selling concentrated at or below that level, macro conditions supportive; that alignment defines a high-quality entry. The thesis is grounded in observable behavior rather than speculation - you are aligning with a strike level that reflects their conviction and getting paid to do it.

The rule is simple: if you are not genuinely willing to own the stock at the strike or you don’t have a very disciplined risk management strategy, do not sell the put. That discipline is what separates this strategy from chasing yield.

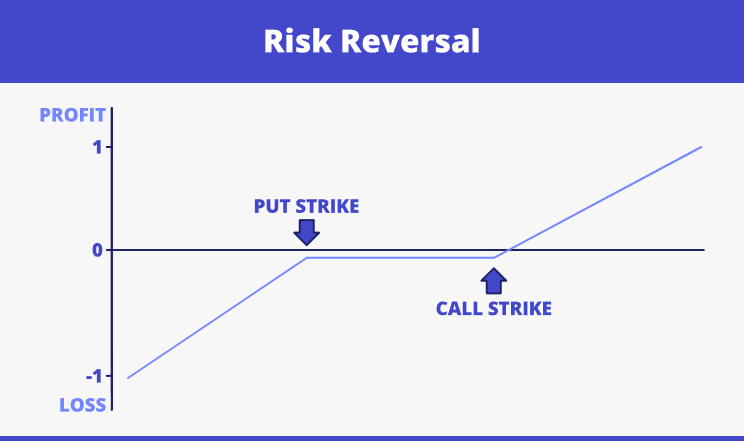

Risk Reversals — Following the Whale or Building Your Own

The risk reversal is a natural extension of the sold put framework. The structure: sell a put, buy a call, typically at equivalent deltas. You are selling what the market chronically overprices - downside puts, which carry a structural premium driven by institutional demand for insurance and buying what it chronically underprices upside calls, depressed by a persistent supply of covered-call sellers.

When this trade comes through the flow in size, it is one of the clearest signals available. A fund putting on a risk reversal is not hedging. It is making a directional statement with a structure specifically designed to take advantage of the volatility skew. When I see it, I have two choices: follow the trade directly, replicating the structure myself, or use the put premium I am already collecting from an existing sold put position to fund the call, adding upside participation at zero additional cost and often for a net credit.

That principle runs through both strategies: always look for a trade where you are being paid to take the position, or where the premium from one leg funds the other. You define your downside at a level where institutions have already signaled their willingness to own the stock. You eliminate your cost of carry on the upside. You align yourself with the best-informed participants in the market.

When implied volatility is elevated, I often prefer a call spread over an outright call. Rather than buying a single call (expensive in a high-vol environment) the spread achieves the same directional exposure at a reduced the cost. The short call within the spread offsets a meaningful portion of the premium paid for the long call, and in most cases that trade-off is worth making. You cap your upside at the short strike, but you substantially reduce or eliminate the net cost of the structure.

The volatility edge underlying both strategies is well documented. Puts are structurally expensive because institutional mandates require hedging but prohibit speculation. That asymmetry means downside premium rarely fully normalizes. Being the disciplined liquidity provider to that demand, on names where the flow, the chart, and the macro backdrop are all aligned, is where the edge compounds over time

How I Track It

Every large structured trade that hits the tape comes through the Options Intelligence dashboard in real time, classified, color-coded and labelled. Sold puts, risk reversals, bull call spreads, rolls, multi-leg structures; every trade type is identified and presented the moment it clears. When I see a name with heavy institutional put selling or a large risk reversal printing in size, I can assess the setup quickly and form my own view.

That is the point of the platform. Not signals. Not tips. The information, decoded, so you can think for yourself with the same clarity that used to require a desk on an options floor.